Depreciation Rules Businesses should know the tax rules for deducting depreciation on a certain property. This deduction can benefit eligible business taxpayers. First off, businesses should remember they can generally depreciate tangible property, except land.

Depreciation Rules Businesses should know the tax rules for deducting depreciation on a certain property. This deduction can benefit eligible business taxpayers. First off, businesses should remember they can generally depreciate tangible property, except land.

Tangible property includes:

- 1) Buildings

- 2) Machinery

- 3) Vehicles

- 4) Furniture

- 5) Equipment

Here are some of the changes to business depreciation under tax reform:

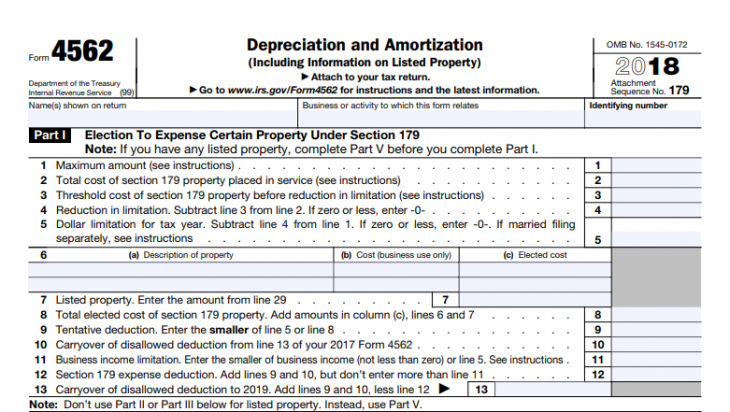

1) Taxpayers can immediately expense more.

2) Businesses may choose to expense the cost of a property and deduct it in the year it is placed in service.

3) The maximum deduction increased from $500,000 to $1 million.

4) The phase-out limit increased from $2 million to $2.5 million.

5) Taxpayers may include improvements made to nonresidential property. The improvements must have been made after the date the property was first placed in service.

These improvements include:

- 1) Changes to a building’s interior

- 2) Roofs

- 3) Heating and air conditioning systems

- 4) Fire protection systems

- 5) Alarm and security systems

Improvements that do not qualify:

- 1) Enlargement of the building

- 2) Service to elevators or escalators

- 3) Internal framework of the building

What is Depreciation?

Depreciation is a “non-cash” expense that reduces the value of an asset over time. When depreciation is non-cash, this means that it is taken as an accounting entry and the amount of cash held by the business is not affected.

Business assets that can be depreciated include equipment, machinery, technology, computers, office furniture, buildings, and improvements to buildings. They include leasehold improvements to a rented property and business vehicles. Land can’t be depreciated because it appreciates instead of depreciating.

Depreciation is taken on business assets to recognize the change in the value of these assets as they age. Assets depreciate for two reasons.

That auto you bought and drove off the lot will decrease in value with every mile and the wear and tear on the engine, the tires, and other components. Assets also decrease in value because they become obsolescent—they are replaced by newer models. Last year’s car model is less valuable because there’s a newer, more desirable version on the market.

These changes apply to property placed in service in taxable years beginning after December 31, 2017.